The new G4 reporting guidelines published by the Global Reporting Initiative are centered on materiality. In order to add to the understanding of this concept, this post explains the importance of materiality and its value in sustainability reporting and strategy.

What is materiality and why is it important?

The concept of materiality has its origins in the auditing and accounting processes of financial reporting. In financial terms, a concept is considered material to the company if its omission or misstatement influences the economic decision of users. In recent years, the concept of materiality has been adopted in sustainability and is increasingly influencing the design of sustainable strategies and reports.

Compared to financial statements, sustainability considers a broader scope of action and covers a multitude of issues- environmental, social, economic and more. This context requires a more comprehensive definition for materiality. The Global Reporting Initiative (GRI) defines as material those issues with “a direct or indirect impact on an organization’s ability to create, preserve or erode economic, environmental and social value for itself, its stakeholders and society at large”.

In simple terms, materiality aims to identify the societal and environmental issues that present risks or opportunities to a company while taking into consideration the issues of most concern to external stakeholders. The process of labeling material topics in a company requires a comprehensive framework that methodologically identifies and prioritizes issues, risks and opportunities, commonly known as materiality analysis.

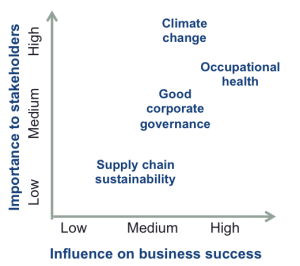

Materiality analysis

Source: PGS Advisors

Source: PGS Advisors

When to perform a materiality analysis?

A materiality analysis is a tool that takes into consideration the company’s financial concerns while foreseeing future risks and opportunities around ESG issues. A materiality analysis is especially useful for companies building a sustainability strategy, preparing a sustainability report or looking to explore new business opportunities.

As in traditional enterprise risk management, strategic planning for sustainability requires a deep understanding of the impacts of a company’s operations and a comprehensive stakeholder map. Materiality analysis helps a company tailor its sustainability strategy and stakeholder engagement activities around the issues that are most pressing to their business and sector. It not only identifies issues with significant social or environmental impact for the company but also takes into account the understanding of stakeholders. When preparing reports, the availability of this information guarantees addressing the issues that represent a major concern to stakeholders and consolidates a company’s accountability strategy.

In addition, materiality analysis can provide information to develop products and services with the greatest potential for sustainable business growth and can influence a company’s decision-making process by weighing risks.

How to identify materiality

Generally, materiality varies considerably from company to company. Material topics can be similar within an industry or a sector, but they also respond to particular characteristics of a company such as size, location, time of establishment, level of stakeholder engagement, financial performance, etc. As a result, the practical application of materiality is constantly evolving. Recently, organizations like the Sustainability Accounting Standards Board (SASB) and the GRI have developed tools to consolidate the process of identifying materiality.

The SASB is in the process of building materiality maps for each industry. It has determined materiality according to issues under five categories: Environmental Capital, Social Capital, Human Capital, Business Model & Innovation, and Leadership & Governance. Until now, materiality maps for the healthcare and financial sector have been published. Maps per industry will be available in the short to medium term.

At the same time, the GRI developed a materiality framework to guide sustainability reporting: the Reporting Guidance for Defining Content in the GRI Sustainability Reporting Guidelines. Companies reporting under these guidelines are taking advantage of the materiality analysis beyond reporting and are using the process to target their sustainability efforts.

Common elements in materiality analysis include:

- Identification of a universe of relevant economic, social, environmental, and governance issues for consideration;

- Evaluation and ranking of the level of stakeholder concern regarding each issue;

- Evaluation and ranking of the potential impact on the company of each issue;

- Presentation of issues prioritization, typically in a matrix format that is subsequently used to inform strategy and reporting.

In addition, the process usually takes into consideration surveys involving consumers and sustainability experts, feedback from stakeholder meetings, engagement events, media scans, internal business impact surveys, corporate risk maps, etc.

Materiality analysis is about setting priorities right. By complementing financial and non-financial performance, materiality helps align a business strategy with a company’s ESG risks and stakeholders’ interests while achieving larger impacts in sustainability. It is quickly becoming the dominant concept in sustainability reporting and it is just a matter of time before companies realize the potential and benefits of a materiality analysis for their overall performance and sustainability in particular.